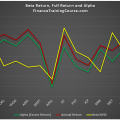

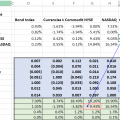

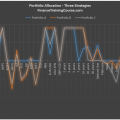

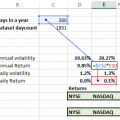

Portfolio Management Alpha dominant strategies. As part of our case discussion in the Portfolio Optimization course this Saturday we proposed a simple question to eighteen odd apprentice Portfolio Managers in the class. We understand how to calculate Beta and Alpha but do we understand how

The post Portfolio Management Alpha dominant strategies. 2012 – 2016 a short case study. appeared first on Finance Training Course.